I've written much on Eurasian Integration, and it's really gone into overdrive with the Ukraine crisis. Here's a new piece for Russia Direct on how Ukraine is killing integration... and how China is benefiting.

|

It's been tough to keep up the blog when everything is going kablowey in Ukraine. but yesterday's crash in Russian markets meant I had to give a lot of commentary on the fly. For your edification, you can check me out here on RT talking about "Black Monday" and here on Dukascopy Swiss Financial TV talking about the same thing (slanted a bit more heavily to interest rates).

Also, I've been fighting twitter trolls who apparently can't quite get that free speech means "you can say what you want" and not "if you don't say things are are unabashedly pro-Russia and anti-Western you are some kind of Nazi and we will track you down at your employer and spam everyone you work with." I think that's the price of fame these days, and I'm not even famous. Russia is a funny place sometimes, but the internet remains the last bastion of nutjobs, wingnuts, trolls, and Stalinist loonies. Either way, enjoy my commentary! Courtesy of Ukraine, which has not just gone off the deep end but is actively attempting to become the poorest nation in Europe, a list of how to completely and utterly botch an economic transition:

Sounds like a perfect recipe, one that Ukraine is following to the letter. Ukraine - the country of the future. Here at IEMS, it's been a hectic day. Apparently all of Russia wants to know about the coming collapse of America and the whole debt battle/government shutdown/dogs and cats living together malarkey that's still ongoing in the US. I gave a short talk to slon.ru (link up when available), my colleague Bill Wilson gave a talk on RT, and both of us have contributed to another online Russian publication. Perhaps not surprisingly, the Russians are eating this up, mainly because the US looks like a big dysfunctional Taiwan (you know, without the stellar growth rates). Of course, as noted on these pages and elsewhere, Russia has nothing to be proud of: onerous bureaucracy, resource dependency, an aging population, and a political culture just above "caveman" leap immediately to mind. But Schadenfreude is powerful in this one.

Oh, and to not give too much away, my own predictions for the rest of the "political crisis" in the US: 1. The Republicans will cave (as usual) 2. Any short-term turmoil will be swamped by the reality of perpetual deficits and an ever-more intrusive state in the long-run 3. Any problems that come from this ever-intrusive state will be blamed on the market. And Republicans. But not for caving. 4. Actually, it's all the fault of the Republicans. Thank you, media! I guess the key takeaway is EVERYBODY PANIC! (just kidding. For the short-term, anyway). In a world where fiscal "austerity" means the growth of government is slowed from 6% annually to 5%, it was perhaps inevitable that governments would still be in dire straits fiscally... and, of course, this means that there need to be new ways to fund Leviathan. The latest approach, pioneered by Central and now Eastern European governments, is a pension grab - either changing the laws to channel private pension fund money into government coffers (as in Poland) or... this. Prime Minister Dmitry Medvedev told ministers Thursday that the government needs to check that the money Russians channel to private pension funds is safe. To do this, it will seize 244 billion rubles ($7.6 billion) from non-state pension funds and put them into the state pension fund.  So to recap, the Russian government is going to "inspect" the money by taking it away, booking it as part of their money for a year, and then possibly giving it back. Does this remind anyone of a Simpsons episode? Also remember, New England Patriots' owner Bob Kraft already claims that Vladimir Putin took his Superbowl ring to "look at" and never gave it back. What is the chance that this money will ever be returned? Even beyond that basic question is a more fundamental one - in what universe this is even considered a half-way decent idea? This shows that the institution of the government only ever operates for one institution, and that is government. In the middle of an economic slow-down such as the one Russia is facing now, the government has decided that keeping the government going is more important than investor confidence, contracts, or any of those either issues that come with a market economy. Here, let me just take that for you! The ramifications of a naked money grab such as this are myriad: decline in the stock market, further deterioration of (admittedly already fragile) property rights in Russia, financial volatility, and a further pallor of economic policy uncertainty. The upside? The government's budget numbers look good for one year. The shortsightedness of government never seems to amaze me.

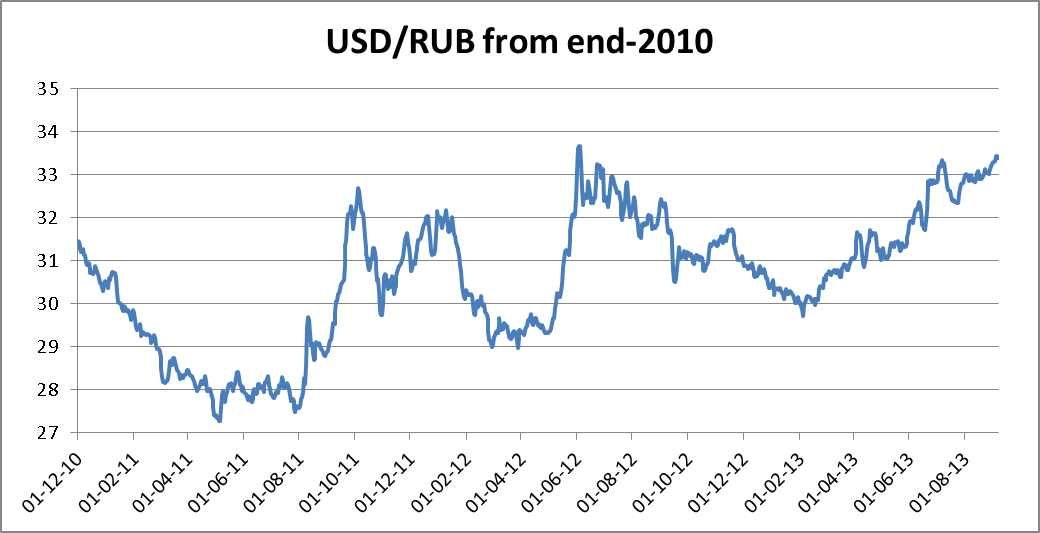

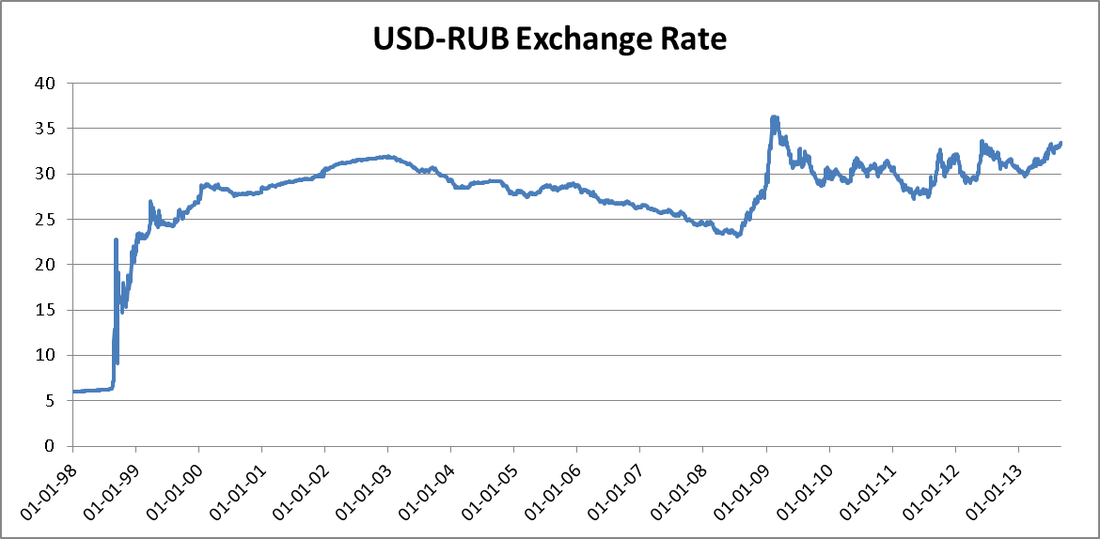

With apologies to Foxy Shazam With apologies to Foxy Shazam Living in Russia, working for an emerging markets think tank, and being paid in rubles, makes you acutely aware of geopolitical tensions, emerging market ripples, and Russia-specific factors. This has been especially true over the summer as, to be polite about it, the ruble plummeted against the US dollar. Now, there's usually a good amount of seasonality for the ruble/USD exchange rate, with drops in the summer due to the lower price of oil and, of course, the fact that the Russians book it out of Moscow as fast as their private jets will take them (meaning more demand for foreign currencies and less for rubles). But this summer, the bottom dropped out:  From just about the 29.8 mark in February, the ruble is now at about 33.40 and climbing daily (with bank premia for foreign exchange, you can sell ruble at about 33.85 this morning with Raiffeisen). That's a loss of 12% (hellooooo depreciated paycheck), not gigantic by historical standards but still a pretty hefty drop in a market where the price of oil hasn't seen major swings. But is this an aberration? Well, yes and no - looking at the Ruble since it became "new" in 1998, we're basically part of a trend that started during the global financial crisis and shows no signs of abating:  So we're not as weak as we were, not as strong as we were, just somewhat bouncing around in the 30-35 range. And this is in line with a general sell-off from emerging markets, as the financial world starts to believe that Ben Bernanke's money spigot won't run forever and "quantitative easing" might actually recede from the US. Russia is just part of a general trend of emerging market pullback.

That's the no, this is not an aberration. But the yes is that, for some reason, the world seems to be waking up to the unsustainable nature of Putin's economy, and we have a big shift in momentum just over the past two months. Putin hasn't helped any, as his new Central Bank head is fairly similar to those in Western countries; i.e. looser monetary policy somehow grows economies magically! And Russia has always been willing to use its economic riches for geopolitical gain (although, as a colleague of mine detailed in RBK Daily earlier this year, the Russian stance on Syria actually caused it some problems with the Saudis, who retaliated by ramping up their oil production to depress prices). The question is, can the almost completely un-diversified Russian economy survive the next round of economic uncertainty? The best part of this is also the bit that makes me so angry - the structure of the Russian economy has been basically frozen in place during Putin's reign, due to uncertain property rights, bureaucratic nightmares (one need only look at Russia's place in Doing Business), and a widespread perception of corruption. And, of course, the institutions needed for a market economy are still fledgling here, subsumed to the formal bureaucratic apparatus of the state. Transaction costs may not have been spawned in Russia, but by golly this place perfected them. So why are traders and the world starting to fret now about Russia? Why is the ruble sliding now? Why have Russia's revised growth estimates suddenly taken the world by storm? Better renegotiate my contract, because I sense that 34-35 rubles to the dollar isn't far off. |

AuthorDr. Christopher Hartwell is an institutional economist and President of CASE Warsaw. All commentary on this page is exclusively his own and in no way represents the views of CASE, his wife, his dog, or anyone else. Especially not his wife or his dog. Archives

July 2014

Categories

All

|

RSS Feed

RSS Feed